There’s nothing more stressful than seeing your business statements show a healthy profit, but your bank account still can’t cover payroll or bills on time.

I’ve definitely felt that headache myself. Unsent invoices pile up, rent is due, and suddenly, running a business feels more like firefighting than anything else.

Cash flow management is one of those topics every small business owner wishes they learned about sooner.

Stick with me here. By the end of this guide, you’ll see cash flow for what it really is and walk away with some super useful ways to keep your business running comfortably, even when revenue hits a bump.

What Is Cash Flow Management for Small Businesses?

Cash flow is just a fancy way of saying “the money moving in and out of your business.”

Cash flow management means making sure you track, plan, and handle this flow of money so you can cover what needs to be paid when it needs to be paid.

It’s not about crunching numbers for tax season.

It’s about knowing day-to-day where your business stands.

There are three basic types of cash flow to know:

- Operating cash flow: This is the money you get from sales and pay out for day-to-day expenses like office rent, supplies, and payroll. Most of your attention will go here.

- Investing cash flow: Money linked to buying or selling equipment, property, or even stocks. For example, if you buy a new delivery van, the payment fits in this part of your cash flow.

- Financing cash flow: Cash you get from loans or investors, plus the money you use to pay off debts or pay back investors.

Keeping these types clear will help you make better decisions and avoid surprises.

Why Cash Flow Management Is More Important Than Profit

It’s easy to think the only number to watch is your profit.

But here’s the reality: profit is just what’s left over after expenses, and it doesn’t always match the cash you actually have ready to spend.

You could show $10,000 in sales this month, but if clients won’t pay until two months from now, you can still run short fast.

Meanwhile, expenses like rent, bills, or even a business insurance premium need to be paid right now.

This is why cash flow touches every part of your business’s survival, since it directly impacts your day-to-day operations.

Related: How to Separate Personal and Business Finances Effectively?

Common Cash Flow Problems Small Businesses Face

If you’ve ever found yourself asking, “Where’d all the money go?” you’re not alone.

These are the pain points that trip up a lot of small business owners:

- Clients pay late: Waiting weeks or months for checks to clear is pretty common, and it can leave you hanging in the meantime.

- Seasonal slumps: Your income spikes in busy months, then drops during the slow season, making budgeting tricky.

- Spending too early on growth: Investing in a bigger space or new team members before you have steady income can put a strain on your cash flow.

- Poor budgeting: Unexpected fees or not tracking regular expenses can drain your account faster than you think.

- Forgetting about taxes: Tax season surprises are the worst, especially if you haven’t been setting that money aside.

Another overlooked issue is not adjusting your expenses during slower periods. If you maintain the same overhead when sales dip, your cash buffer can vanish quickly. Also, relying on a single major client can cause issues if their payments are delayed.

Related: What Are the Basic Bookkeeping Concepts Every Small Business Owner Should Know?

8 Practical Cash Flow Management Strategies for Small Businesses

- Forecast Your Cash Flow Monthly

Look ahead and estimate your income and your regular or one-off expenses each month. This helps you spot any trouble before you run out of money and scramble for a solution. Even a simple spreadsheet works, but cloud-based tools make it even easier to track from anywhere. - Shorten Your Payment Cycles

Send invoices as soon as you wrap up a job, don’t wait for “invoicing day.” You can also offer a small discount for clients who pay early and be clear about your payment terms upfront, such as “Net 15” or “Due on Receipt.” Consider sending gentle email reminders a few days before payment is due to avoid late payments. - Separate Tax Money Immediately

Every time money comes in, move a set percentage (like 20-30%) into a savings account for taxes. This way, the money’s there when you need it, and you’re not surprised at year-end. - Build a Business Emergency Fund

Shoot for saving two or three months’ worth of expenses. This is your buffer during slow stretches so you don’t have to borrow at the worst time. - Control Recurring Expenses

Look at every subscription or automatic payment every few months. If you’re not using certain tools or you can find a cheaper option, cut them loose. There’s no point paying for things you rarely use. Even reviewing your utility bills and renegotiating contracts can make a difference. - Monitor Cash Flow Weekly (Not Just Monthly)

Spend ten minutes every week reviewing who owes you money, any upcoming bills, and checking your balances. This regular habit helps you avoid scary surprises or last-minute panic. Weekly check-ins make it easy to adjust if something unexpected comes up. - Avoid Mixing Personal and Business Spending

Keep separate accounts, and run all your spending through the business account only. This keeps bookkeeping cleaner and makes it easier to see what’s really going on. It also helps you stay organized and makes tax time a lot smoother. - Reinvest Strategically, Not Emotionally

Growth is great, but every dollar you invest should have a plan and a goal. Resist the urge to overextend unless you know it fits your cash flow forecast. Liquidity, meaning the amount of available cash, is what keeps you going when things get tough. Use your extra cash to upgrade wisely and avoid large purchases that aren’t urgent.

Bonus tip: Negotiate better payment terms with vendors when possible, like longer payment windows, which can help stretch your cash even further.

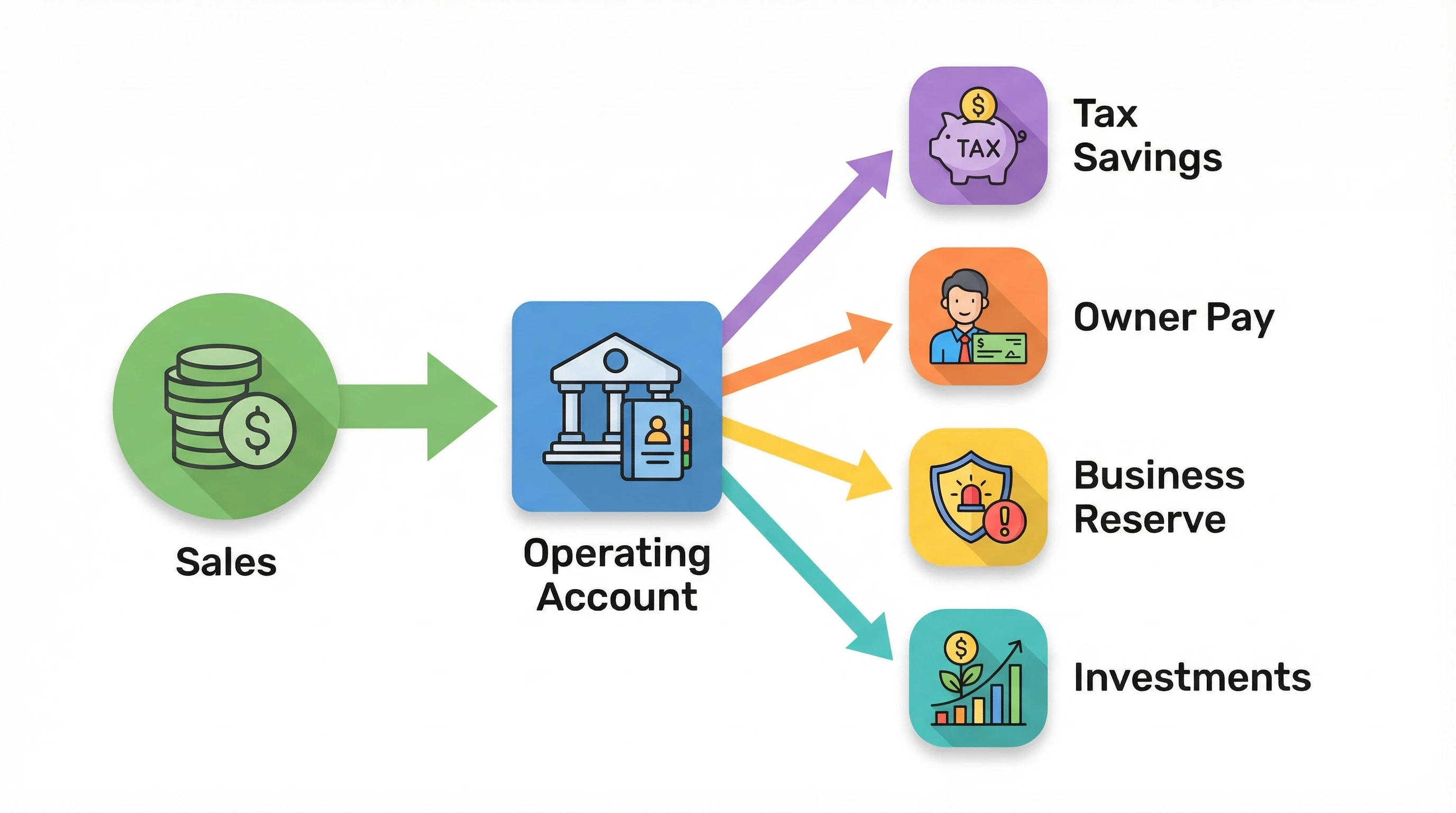

Simple Cash Flow System for Online Entrepreneurs

Here’s a basic system I use that works for almost any solo business owner:

- All sales go straight to one main operating account.

- Every payday, move your tax percentage to a separate savings account.

- Pay yourself regularly (owner pay). Don’t just take random withdrawals.

- Set up a reserve fund for emergencies from each payment.

- The leftover funds can then be used to reinvest into the business or saved for bigger purchases or investments.

This structure makes it clear where your money goes after each sale, and it stops everything from getting mixed up. For many online entrepreneurs, automating transfers with online banking can help enforce this routine without any hassle. If you use digital products or services as part of your business, consider linking them to your operating account only, further simplifying tracking and budgeting.

Mistakes That Kill Small Business Cash Flow

- Assuming that sales revenue means you’ve got plenty of cash to spend right now

- Forgetting to account for taxes (seriously, happens way too often)

- Scaling up with big expenses before you’re truly ready

- Using credit cards or business loans to plug every gap

- Not reviewing your numbers regularly. If you’re only looking at statements at tax time, you’re missing warning signs months in advance

- Ignoring the small fees and charges that slowly eat away at your balance, such as payment processor fees

Plus, be wary about spending on new business trends or tools just because they seem popular. Always double-check that your business genuinely needs them before signing up.

Frequently Asked Questions

Q: Is cash flow the same as profit?

No. Profit is what’s left over after expenses, but cash flow tracks when the money actually moves in and out. You can have profit, but if customers pay slowly or expenses are due now, you might still be short on cash.

Q: How much cash reserve should a small business have?

It’s smart to aim for two to three months of operating expenses set aside. It’s enough of a cushion to cover slow months or an emergency. In fast-changing industries, you might decide to save a bit more if your income is extra unpredictable.

Q: How often should I review my cash flow?

I recommend a quick review every week to catch issues early and a deeper jump in at the end of each month to spot patterns or make adjustments.

Want to Build a Business That Generates Predictable Income?

Knowing how to manage cash flow is just the beginning. If you’re serious about creating predictable, steady income—not just short bursts—you need a solid business and income system in place.

I’ve tested a bunch of different online business models, and one training platform in particular stands out for teaching not just how to make money, but how to keep it organized and growing.

Explore my #1 recommended platform and start building your sustainable online income the right way.

The name of this training platform is Wealthy Affiliate. I joined it back in 2015, when I was first looking to build a second income, and to this day, I am still with them.

Free Access to the STARTER MEMBERSHIP which includes:

- 8-lesson core niche training

- WA help/community access (2.5 + million members)

- 7 days of coaching/mentoring from me

- And more…

Go ahead and check out my detailed Wealthy Affiliate review here, or create your free STARTER account here.

Talk to you soon.

Regards

Roopesh